ES

ES  RU

RU  TR

TR  FA

FA  AR

AR  ZH

ZH Blog

Blog description

Secondary OFAC Sanctions - Enforcement Trends, Case Studies, and Exposure of Non-U.S. Companies

Over the past decade, especially after the expansion of Russia-related measures in 2022, secondary sanctions have moved from a niche concept to a central pillar of U.S. economic enforcement. Unlike traditional sanctions, which are largely tied to jurisdictional limits, secondary sanctions reach beyond U.S. borders.

They can expose non-U.S. companies, financial institutions, intermediaries, and entire trade networks to significant legal, financial, and commercial risk.

What makes secondary sanctions particularly powerful is not just their legal scope, but how they are enforced. Rather than relying only on direct penalties, the U.S. leverages the central role of its financial system to apply pressure indirectly but effectively.

In practical terms, this creates a stark choice for non-U.S. actors: align with U.S. sanctions expectations or risk losing access to global markets, correspondent banking relationships, and the financial infrastructure that underpins international business.

I. Concept and Legal Basis of Secondary Sanctions

Secondary sanctions are measures imposed by the United States, primarily through the Office of Foreign Assets Control (OFAC), that target non-U.S. persons for engaging in certain transactions involving sanctioned countries, entities, sectors, or individuals.

These authorities are grounded in a mix of statutes and executive powers, including:

- the International Emergency Economic Powers Act (IEEPA)

- the Countering America’s Adversaries Through Sanctions Act (CAATSA)

- country-specific Executive Orders, such as Executive Order 14024

What sets secondary sanctions apart is what they don’t require. Unlike primary sanctions, there is no need for a direct U.S. connection: no U.S. persons, no U.S. territory, and not even a U.S. dollar transaction.

Instead, they work through indirect pressure. The real leverage comes from the potential loss of access to:

- U.S. correspondent banking relationships

- U.S. dollar clearing systems

- the broader global financial infrastructure shaped by U.S. regulatory standards

In effect, secondary sanctions extend U.S. influence far beyond its borders by making access to the financial system itself conditional on compliance.

II. Enforcement Mechanisms: Financial Leverage Over Jurisdiction

Secondary sanctions are enforced through three primary mechanisms:

1. SDN Designation

Non-U.S. entities can be placed on the Specially Designated Nationals (SDN) List maintained by the Office of Foreign Assets Control. This typically results in:

- Blocking of any property within U.S. jurisdiction

- Immediate termination of relationships with international banks

- Significant reputational damage

While the legal effect is tied to U.S. jurisdiction, the practical impact is global. Most banks and counterparties simply will not take the risk of dealing with an SDN-listed entity.

2. Correspondent Banking Restrictions

Foreign financial institutions may be restricted, or cut off entirely, from:

- maintaining correspondent accounts in the United States

- operating payable-through accounts

In real terms, this can mean losing access to U.S. dollar clearing, which remains critical for international trade, cross-border payments, and day-to-day global banking operations.

3. Sectoral Sanctions

These measures target entire industries rather than specific entities. They can limit:

- access to financing, including debt and equity markets

- transfers of technology

- provision of key services

Sectoral sanctions are especially impactful in industries like energy, defense, finance, logistics, and other strategically important supply chains, where access to capital, technology, and services is essential to operate.

III. Triggering Conduct: Legal Standards in Application

A. “Significant Transactions”

Secondary sanctions often turn on whether a non-U.S. person has engaged in a “significant transaction” with a sanctioned party.

The Office of Foreign Assets Control (OFAC) applies a multi-factor analysis, typically looking at:

- the size and value of the transaction

- the frequency and pattern of activity

- the nature of the goods or services involved

- the strategic importance of the transaction

- the level of awareness or knowledge

There is no fixed monetary threshold. That lack of a bright line creates real uncertainty for non-U.S. companies and financial institutions trying to assess risk in advance.

B. Material Support and Facilitation

Exposure is not limited to direct transactions. Liability can arise from providing:

- financial services

- logistical support

- brokerage or intermediary functions

- technical or advisory assistance

In practice, this means a company does not need to deal directly with a sanctioned party to face risk. Indirect involvement, i.e. facilitating, supporting, or enabling a transaction can be enough.

C. Sanctions Evasion and Circumvention

Recent enforcement trends show a clear focus on how transactions are structured, not just who is involved. Common risk patterns include:

- transshipment through third countries

- use of layered or opaque corporate structures

- re-labeling or misclassification of goods

This reflects a broader shift in enforcement: regulators are increasingly targeting entire evasion networks and trade ecosystems, rather than just individual actors.

IV. Case Studies and Enforcement Practice

1. EFG International (Switzerland, 2024)

A Swiss financial institution processed transactions linked to a sanctioned Russian individual through omnibus account structures that obscured beneficial ownership.

Outcome: Enforcement action and financial penalty.

Implication: Even sophisticated institutions face exposure when beneficial ownership controls, account transparency, and escalation procedures fall short.

2. UAE-Based Trading and Logistics Networks (2024–2025)

Multiple entities in the United Arab Emirates were designated for facilitating trade on behalf of sanctioned Russian parties, often through re-export schemes, procurement networks, and layered intermediary structures.

Implication: Third-country intermediaries, especially in major global trade hubs, have become primary enforcement targets.

3. Multi-Jurisdiction Designations under EO 14024 (2025)

U.S. authorities designated more than 150 entities across multiple jurisdictions for supporting Russia’s military-industrial base and broader sanctions evasion networks under Executive Order 14024.

Implication: Enforcement has moved beyond isolated actors to network-based targeting, capturing suppliers, logistics providers, financial intermediaries, and procurement facilitators.

4. Banking Sector De-Risking (China, UAE, Turkey)

Financial institutions in jurisdictions such as China, the United Arab Emirates, and Turkey began restricting or delaying Russia-related transactions due to perceived secondary sanctions risk.

Implication: Banks are increasingly acting as de facto enforcement gatekeepers, often tightening controls before regulators formally act.

5. Fintech and Alternative Financial Systems (2024)

Certain fintech platforms were designated for enabling alternative payment channels designed to circumvent sanctions restrictions.

Implication: Secondary sanctions now extend into digital financial infrastructure, including fintech platforms, payment systems, and emerging technologies, not just traditional banking.

V. The OFAC 50 Percent Rule: Indirect Exposure

Under OFAC guidance, any entity owned 50% or more, individually or collectively, by sanctioned persons is itself treated as blocked.

Practical Consequences

- Entities may be subject to sanctions even if they are not expressly listed

- Ownership aggregation requires detailed analysis

- Investment funds, lenders, insurers, and counterparties face hidden exposure risks

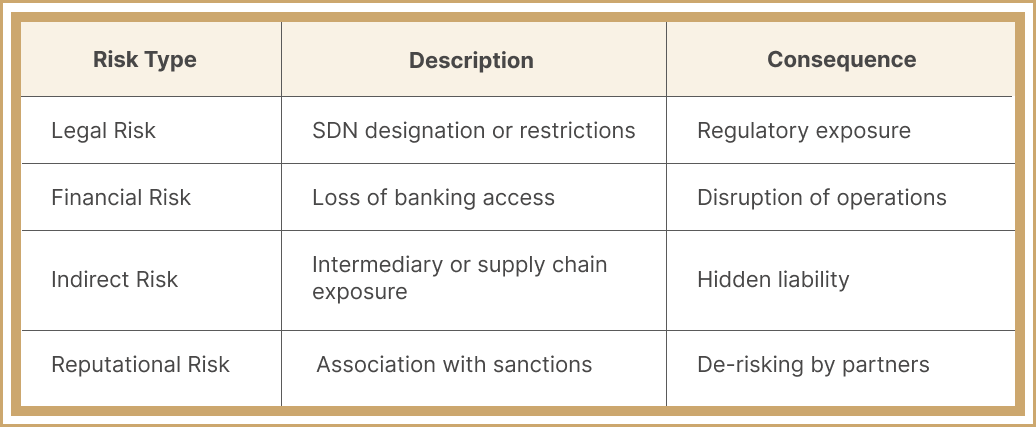

VI. Risk Profile for Non-U.S. Companies

Secondary sanctions create a multi-layered risk environment:

VII. Compliance Considerations

A robust sanctions compliance framework for non-U.S. companies exposed to secondary OFAC risk must move beyond basic screening and adopt a multi-layered, risk-based control architecture. The objective is not only to identify direct exposure, but also to detect indirect, structural, and transactional risk vectors that are the primary focus of modern enforcement.

1. Beneficial Ownership Analysis (Beyond Formal Ownership)

A compliant framework requires granular transparency into ownership and control structures, including indirect and aggregated interests.

Core Elements:

Ultimate Beneficial Owner (UBO) Identification

- Map ownership chains across jurisdictions

- Identify natural persons and controlling entities

Application of the OFAC 50 Percent Rule

- Aggregate ownership across multiple sanctioned persons

- Assess both direct and indirect ownership

Control Analysis (Beyond Equity)

- Voting rights

- Board control

- Contractual influence

Dynamic Monitoring

- Periodic refresh of ownership data

- Trigger-based reviews, including mergers, acquisitions, restructurings, and shareholder changes

Practical Risk:

Sanctions exposure often arises where ownership is fragmented across multiple entities, each below 50 percent, but collectively exceeding the threshold.

2. Transactional Risk Assessment (Substance Over Form)

A defensible compliance program must assess not only counterparties, but also the nature, purpose, and economic substance of transactions.

Key Analytical Factors:

Transaction Value and Frequency

- Large or recurring transactions increase risk

Nature of Goods or Services

- Dual-use goods

- Energy-related goods and services

- Financial services

Economic Purpose

- Whether the transaction supports a sanctioned sector, activity, or person

Counterparty Role

- Direct versus intermediary involvement

Awareness / Red Flags

- Unusual structuring

- Last-minute changes in routing or counterparties

Advanced Controls:

- Pre-transaction legal review for high-risk deals

- Risk scoring models for transaction approval

- Escalation thresholds for “significant transaction” analysis

3. Supply Chain Due Diligence (End-to-End Visibility)

Modern enforcement focuses heavily on supply chain participation, including indirect facilitation.

Required Measures:

Counterparty Mapping

- Identify all participants in the transaction chain

- Suppliers, distributors, freight forwarders, and agents

Geographic Risk Analysis

- High-risk jurisdictions, including the UAE, Turkey, and the CIS

- Transshipment hubs

Goods Tracking

- Origin and destination verification

- End-use and end-user certifications

Contractual Safeguards

- Sanctions compliance clauses

- Audit rights

- Termination triggers

Red Flags:

- Use of intermediaries with no clear economic function

- Routing through high-risk jurisdictions without justification

- Discrepancies in shipping or customs documentation

4. Financial Controls (Payment and Banking Risk Management)

Financial flows are a primary enforcement vector. Controls must address both direct and indirect payment exposure.

Core Components:

Payment Flow Mapping

- Identify all banks and intermediaries involved

- Monitor correspondent banking relationships

Currency and Routing Analysis

- Even non-U.S. dollar transactions require scrutiny

- Identify indirect exposure through clearing chains

Banking Relationship Management

- Understand counterparties’ compliance expectations

- Anticipate de-risking behavior

Screening of Financial Intermediaries

- Not only clients, but also banks and payment processors

Advanced Controls:

- Real-time transaction monitoring systems

- Payment blocking and escalation protocols

- Pre-clearance for high-risk payments

Practical Reality:

Banks frequently act as first-line enforcers, blocking transactions before regulators intervene.

5. Internal Governance and Compliance Infrastructure

An effective compliance system must be embedded at the organizational level and supported by clear governance structures.

Structural Elements:

Sanctions Compliance Program

- Written policies aligned with OFAC guidance

- A risk-based approach tailored to the business model

Dedicated Compliance Function

- A sanctions officer or team

- Direct reporting lines to senior management

Training and Awareness

- Role-specific training for legal, finance, and operations personnel

- Regular updates based on enforcement trends

Escalation and Reporting Mechanisms

- Internal reporting channels

- Documented decision-making processes

Audit and Testing

- Periodic internal audits

- Independent reviews of compliance effectiveness

6. Third-Party Risk Management (Critical Enhancement)

Given the enforcement focus on intermediaries, companies must actively manage third-party risk.

Required Actions:

- Due diligence on:

- Agents

- Distributors

- Consultants

- Logistics providers

- Ongoing monitoring, rather than one-time onboarding

- Contractual representations and warranties

- Risk-based segmentation of third parties

7. Documentation and Defensibility

In an enforcement scenario, documentation is critical.

Maintain:

- Due diligence records

- Transaction risk assessments

- Internal approvals and escalation logs

- Compliance program documentation

Objective:

Demonstrate a good-faith, risk-based compliance effort, which is a key mitigating factor in enforcement.

8. Integration with Export Controls and AML

Secondary sanctions risk often overlaps with:

- Export controls, including the EAR and ITAR

- Anti-money laundering (AML) frameworks

An effective program should integrate:

- Screening systems

- Risk assessment methodologies

- Reporting structures

VIII. Structural Implications for Global Commerce

Secondary sanctions represent a shift from jurisdiction-based regulation to system-based enforcement.

Their effectiveness derives from:

- The central role of the U.S. financial system

- The risk aversion of global financial institutions

- The integration of legal and market-based enforcement

As a result, non-U.S. companies are increasingly regulated not by formal jurisdiction alone, but by their access to global financial infrastructure.

Frequently Asked Questions (FAQ)

What are secondary OFAC sanctions?

They are U.S. measures targeting non-U.S. companies for certain dealings with sanctioned parties, even in the absence of a traditional U.S. nexus.

Do they apply without U.S. dollar transactions?

Yes. Currency is not determinative.

What is a “significant transaction”?

It is a fact-specific determination based on multiple qualitative and quantitative factors.

Can indirect involvement trigger sanctions?

Yes. Facilitation and intermediary roles may be sufficient.

What is the most severe consequence?

Loss of access to correspondent banking and global financial systems.

How does the 50 Percent Rule work?

Entities owned 50 percent or more by sanctioned persons are treated as blocked.

IX. Conclusion

Secondary OFAC sanctions have fundamentally reshaped the global compliance landscape. Their extraterritorial reach combined with the leverage of the U.S. financial system makes them one of the most powerful tools of modern economic policy.

For non-U.S. companies, the takeaway is straightforward:

Sanctions compliance is no longer a peripheral legal concern. It is a core strategic requirement for participating in international markets.